How do avoid student debt relief scams

Repaying your student loans is stressful enough without having to worry about avoiding scams that may end up costing you more money. Here are some helpful tips to steer you clear of scams trying to cash in on your student loan repayment.

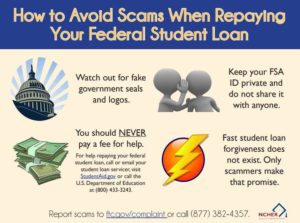

- You don’t need to pay anyone other than your loan servicer – If a company offers to facilitate your student loan repayment but wants to take a portion of your payment it’s probably a scam. Students can call their loan servicers or the US Department of Education directly for options involving income based repayments and loan consolidation at no cost to the borrower. Students can call 1-800-557-7392 or visit studentaid.ed.gov for more information

- You don’t need to pay up front – You should avoid any company looking for upfront payment prior to performing any services. This is especially true for companies involving student aid. You do not need to pay anyone to apply for student aid and you don’t need to pay anyone else to facilitate your repayment of your student aid.

- If it seems too good to be true it probably is – Student loan forgiveness does exists but it is set by federal laws and not subject to negotiation. Same is true for repayment levels. If a company offers to have the ability to negotiate a cancellation or debt relief after a certain level of payments then they are trying to scam you out of your money.

- False affiliations – Avoid companies that try to appear to be affiliated with the government but aren’t actually affiliated. You can speak directly to the US Department of Education about your student loans at 1-800-557-7392 or visit online at studentaid.ed.gov.

- Don’t sign power of attorney or a third party authorization – You made it through school, you can handle this. You don’t need to sign over power of attorney over your student loan debt to anyone. And since you can deal directly with the US Department of Education there’s never any reason for a third party authorization.

Student loan repayment is serious and can be stressful but it doesn’t have to be. If you stay connected with your loan servicer with an online account you can stay on top of your student loan payment due dates, amounts, and options when you’re having trouble making the payments.

Your loan servicer can direct you to programs that can tailor your monthly payment to your income or help you defer payments during times of unemployment or other scenarios.

You can check your student loan history by visiting www.nslds.ed.gov .

Here is a list of the current loan servicers working with the US Department of Education. If you’re contacted by a company not on this list then you should not provide any of your personal information.

You can log into My Federal Student Aid at www.studentaid.ed.gov to find out where to make your student loan payments and what company services your loans.

If you don’t have an FSA ID (username and password) or forgot yours you can create or retrieve it by visiting www.fsaid.ed.gov.